GCC Seafood Market Analysis

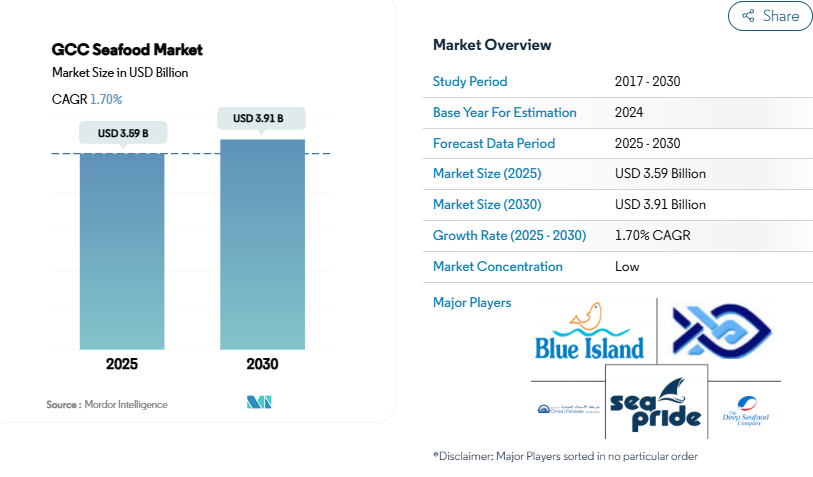

The GCC Seafood Market size is estimated at 3.59 billion USD in 2025, and is expected to reach 3.91 billion USD by 2030, growing at a CAGR of 1.70% during the forecast period (2025-2030).

The GCC seafood industry is experiencing significant transformation driven by changing demographics and consumer preferences. Nearly 90% of the UAE’s population consists of immigrants, with Indians comprising over 40%, followed by Indonesians and Bangladeshis, contributing to diverse culinary preferences and increased seafood consumption. This demographic diversity has led to a surge in demand for various seafood products, particularly in urban areas where international cuisine is highly popular. The rising health consciousness among consumers, coupled with the concerning obesity rates exceeding 25% in countries like Kuwait and Saudi Arabia as of 2023, has further accelerated the shift towards fish and seafood as a healthier protein source.

Infrastructure development and cold chain logistics are playing crucial roles in market expansion. In 2023, A.P. Moller-Maersk strengthened its presence in the UAE by opening a new cold storage facility in Dubai South, increasing its total capacity by 70%. This development is complemented by the establishment of one of the most technologically advanced warehouses in the GCC in Abu Dhabi. These investments are essential for maintaining product quality and extending shelf life, particularly in the region’s challenging climate conditions. The improved storage and distribution capabilities have enabled retailers to maintain consistent supply and expand their product offerings.

The foodservice sector is witnessing remarkable growth, driven by expanding restaurant chains and changing consumer dining preferences. In 2023, UAE-originated seafood chain Golden Fork announced plans to open 20 more outlets across the country by 2024, demonstrating the robust demand for seafood in the dining sector. The restaurant industry’s expansion is supported by government initiatives, including financial aid and tax relief programs, which have helped stabilize the sector and encourage innovation in seafood cuisine offerings.

Sustainability and local production initiatives are gaining momentum across the GCC region. The UAE government’s commitment to supporting local fisheries was evident in 2022 when it awarded subsidies to 500 fishermen to enhance domestic production capabilities. The focus on sustainable fishing practices and aquaculture development is reshaping the industry’s future, with governments implementing various support measures to ensure long-term viability. This shift towards sustainability is particularly relevant given the region’s increasing focus on food security and self-sufficiency, with several countries implementing comprehensive programs to boost local seafood production while maintaining environmental standards.

GCC Seafood Market Trends

Self-sufficiency initiatives implemented by governments are anticipated to grow with production

- Saudi Arabia is the largest fish producer in the Middle East, producing 446,977 tons of fish in 2022. Fish production in Saudi Arabia increased by 6.48% from 2017 to 2022, followed by the United Arab Emirates, with 287091.9747 tons in 2022. Fish production increased gradually from 2021 to 2022, mainly due to the government’s focus on fisheries. Governments are boosting opportunities to involve the private sector in fisheries. A unique program, the National Fisheries Development Program, aims to enhance the fisheries sector’s contribution to GDP and increase the productivity of the aquaculture sector to 600 thousand tons in stages from 15 years to 2030. Regional centers for fishing academies have also been established to support fisheries. Over USD 80 million was invested in the research activities of fish to enhance production capabilities.

- Countries like the UAE have the highest annual per capita fish consumption in the Gulf Cooperation Council (GCC), which is nearly 50% higher than the global average. Despite rapid economic growth, the UAE’s local fisheries are overfished, and local fish account for only 8% of UAE consumption.

- Fish production is projected to increase sustainably from 2023 to 2029. Support from the private sector and identification of fisheries for enhanced development, new partnerships with stakeholders and subsidies for fisheries, and the development of 3,000 fisheries with resource persons may help increase the production and productivity of fisheries from 2022. For instance, in 2021, NEOM Company and Tabuk Fish Company signed a memorandum of understanding to expand local aquaculture production and apply the new generation of aquaculture technologies in the NEOM region of Saudi Arabia.

High dependency on imports raises prices

- In 2022, the United Arab Emirates had the highest fish prices compared to Saudi Arabia and the Rest of Middle East, with the price difference being around USD 4,022 per ton. The difference was mainly due to more subsidies on fuel, infrastructure, and other associated costs by the Saudi Arabian government. The country has the added advantage of a 2,640 km coastline. The retail price range for fish in the United Arab Emirates in June 2023 was between USD 4 and USD 20 per kilogram or between USD 1.81 and USD 9.07 per pound (lb).

- The prices in the Middle East increased due to high demand, which exceeded the supply. The local fish supply decreased, and local production was hampered due to unfavorable climatic conditions in 2020 and 2021. The daily auctions for fish sales by fishermen enable buyers to strike good deals and resell their goods at higher prices, thus directly increasing retail consumer fish prices.

- From 2021 to 2022, fish prices increased by around 0.96%, from USD 3,043 to USD 3,072. The rising fish prices are due to increasing oil prices and rising inflation. To curb this increase, the governments are launching relief measures. For instance, in 2022, the UAE government doubled the budget to support low-income families in the country. Another instance is when the king of Saudi Arabia announced USD 5.33 billion for direct cash transfers and stockpiling in 2022.

- Fish prices are expected to record a sustainable growth rate during the forecast period (2023-2029). Several public and private partnerships are undertaken to enhance the production of fisheries in the Middle East. Saudi Arabia spent USD 80 million on research and planning to develop fish cultivation inland with master trainers to increase production, which is anticipated to help with constant prices.

OTHER KEY INDUSTRY TRENDS COVERED IN THE REPORT

- Increasing production initiatives to stabilize prices during the forecast period

Segment Analysis: Type

Fish Segment in GCC Seafood Market

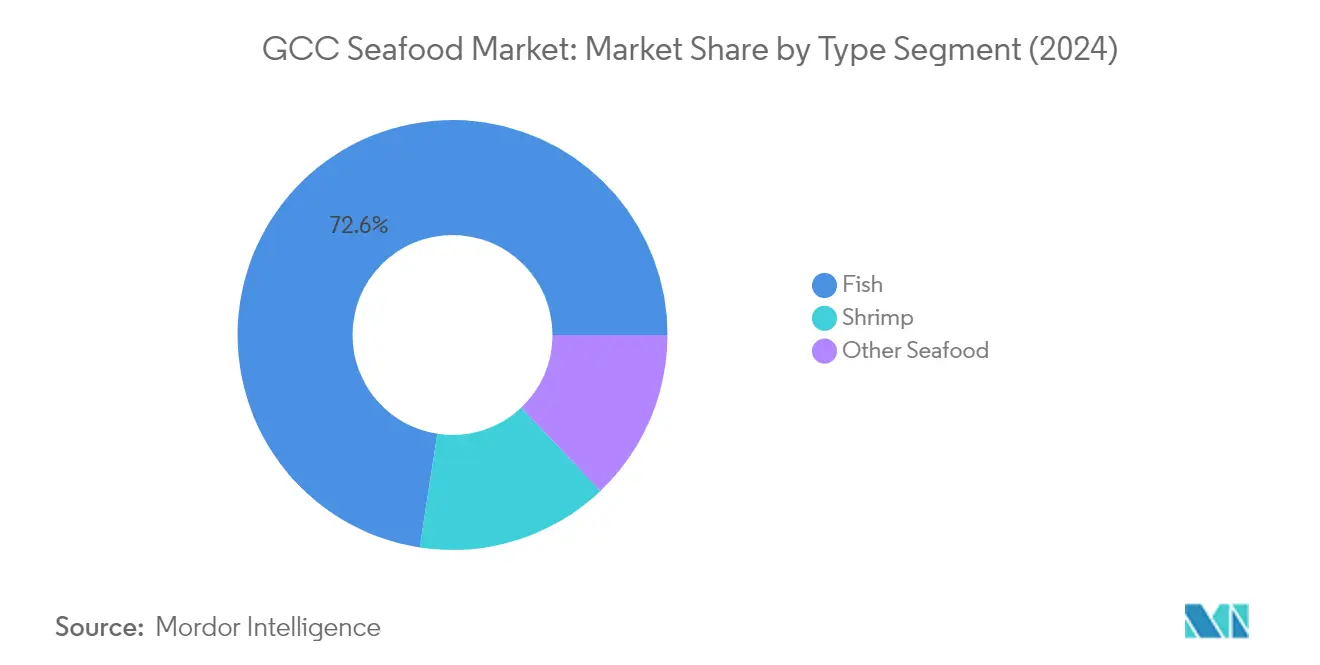

Fish dominates the GCC seafood market, commanding approximately 73% market share in 2024, establishing itself as the cornerstone of the regional fish and seafood industry. The segment’s prominence is driven by the perennial usage of fish as part of traditional Middle Eastern cuisine, with popular variants including salmon, tilapia, and cod being widely consumed across the region. The United Arab Emirates has emerged as a significant market for fish products, with more than 66% of residents consuming fresh fish at least once or twice a week. The country’s strategic geographical location and financial incentives, such as 100% foreign ownership and favorable tax policies, have contributed to the development of its aquaculture industry. Additionally, technological advancements in bio systems that recycle water and nutrients have enhanced the sustainability of fish production while minimizing environmental impact.

Shrimp Segment in GCC Seafood Market

The shrimp segment is projected to exhibit the strongest growth in the GCC seafood market, with an anticipated growth rate of approximately 3% during 2024-2029. This growth trajectory is primarily supported by increasing regional government efforts to boost local shrimp production across Bahrain, Saudi Arabia, UAE, and other GCC nations. The market expansion is further driven by the rising number of shrimp-based product launches and growing consumer awareness of shrimp’s health benefits. The United Arab Emirates has demonstrated significant commitment to shrimp cultivation, exemplified by Prime Aquaculture FZE and Jebel Ali Free Zone’s partnership to establish the region’s first shrimp recirculating aquaculture system farm, designed to produce over 1,000 MT of shrimps annually. The segment’s growth is also bolstered by consumers shifting toward protein-rich diets, driven by strong economic growth and increased health consciousness in the region.

Remaining Segments in GCC Seafood Market

The other seafood segment, encompassing products such as lobsters, crabs, and oysters, plays a vital role in diversifying the GCC seafood market offerings. This segment caters to the premium market segment, particularly in luxury dining establishments and high-end retail outlets. The demand for these premium seafood products has been notably strong in the tourism and hospitality sectors, especially in countries like the UAE and Saudi Arabia. The segment has witnessed increased imports of high-value seafood products such as scallops, lobsters, and caviar, driven by the expanding economy and flourishing tourism industry. The availability of mud crabs, known for their high flesh content and rapid growth rate in captivity, has particularly enhanced the segment’s appeal to consumers seeking diverse seafood options.

Segment Analysis: Form

Fresh/Chilled Segment in GCC Seafood Market

The fresh and chilled seafood segment dominates the GCC seafood market, commanding approximately 57% market share in 2024. This significant market position is primarily driven by the region’s strategic location surrounded by seven seas, providing abundant access to fresh seafood sources. The United Arab Emirates leads consumption in this segment, with fresh and chilled variants occupying nearly 57% market share due to their extensive usage in traditional Middle Eastern dishes like Sayadieh, Pilaf, and Ghraybeh. The segment’s dominance is further strengthened by the growing population’s preference for protein-rich, direct farm-raised products, with consumers willing to pay 30-40% higher prices for fresh/chilled seafood due to high disposable income in the region, which is approximately 2-3 times the global average.

Processed Segment in GCC Seafood Market

The processed seafood segment is emerging as the most dynamic category in the GCC seafood market, projected to grow at approximately 4% CAGR from 2024 to 2029. This accelerated growth is driven by the increasing number of working professionals seeking convenient meal solutions, particularly in the UAE where the women employment rate reached 35% in 2024. The segment’s expansion is supported by rising consumer interest in processed seafood products due to their longer shelf life and reduced frequency of retail outlet visits. The growth is further bolstered by the region’s dependence on seafood imports from countries like Korea, India, and Bangladesh, who are introducing innovative processed variants including fish, shrimp, lobsters, salmon, and tuna products to meet the evolving consumer preferences.

Remaining Segments in Form Segmentation

The frozen and canned segments complete the GCC seafood market’s form segmentation landscape. The frozen segment maintains a strong presence in the market, particularly through the on-trade channel, offering convenience for foodservice establishments and eliminating the need for frequent fresh seafood deliveries. The segment’s growth is supported by expanding cold chain logistics infrastructure, with major players like A.P. Moller-Maersk establishing advanced cold storage facilities in the region. Meanwhile, the canned segment serves specific market needs, particularly in military bases and remote locations, offering longer shelf life and convenient storage solutions while maintaining nutritional value. Both segments benefit from the region’s well-developed retail infrastructure and growing consumer acceptance of preserved seafood products.

Segment Analysis: Distribution Channel

On-Trade Segment in GCC Seafood Market

The on-trade distribution channel dominates the GCC seafood market, commanding approximately 55% of the total market value in 2024. This significant market share is primarily driven by the expansion of seafood restaurant chains across the region and growing consumer preference for dining out experiences. The segment’s strong performance is supported by the increasing number of tourists visiting the region for luxury dining experiences in multi-cuisine restaurants. The demand for full-service restaurants is particularly strong in countries like the UAE, where fine dining establishments such as Aseelah, Al Fanar Restaurant, and Zaman Awal offer authentic regional cuisines featuring premium seafood dishes. The segment’s growth is further bolstered by the rising number of seafood-specific restaurant chains and their expansion plans across the GCC region.

Off-Trade Segment in GCC Seafood Market

The off-trade channel is projected to be the fastest-growing segment in the GCC seafood market, with an expected growth rate of approximately 3% during 2024-2029. This growth trajectory is primarily driven by the rapid evolution of e-commerce platforms and increasing internet penetration in the region, which reached nearly 84% in 2023. The segment’s expansion is further supported by the growing consumer preference for convenient shopping options and the increasing adoption of online grocery delivery services. Major retailers are actively expanding their digital presence and cold storage facilities to meet the rising demand. For instance, Amazon’s new warehouse in Dubai South has increased its total capacity in the UAE by 70%, while its Abu Dhabi facility is positioned to be one of the most technologically advanced warehouses in the GCC region. The segment’s growth is also fueled by the increasing number of supermarkets and hypermarkets offering diverse seafood products and the rising popularity of convenience stores providing ready-to-cook seafood options.

Remaining Segments in Distribution Channel

Within the off-trade channel, various sub-segments play crucial roles in shaping the market dynamics. Supermarkets and hypermarkets serve as primary retail points, offering a wide range of fresh, frozen, and processed seafood products. Convenience stores cater to immediate consumer needs with their strategic locations and focused product offerings. The online channel is revolutionizing seafood retail through e-commerce platforms and mobile applications. Other distribution channels, including traditional fish markets and specialty seafood stores, continue to serve specific consumer segments with their unique value propositions. Each of these channels contributes to the market’s overall growth by catering to different consumer preferences and shopping behaviors across the GCC region.

GCC Seafood Market Geography Segment Analysis

GCC Seafood Market in United Arab Emirates

The United Arab Emirates dominates the GCC seafood market, holding approximately 38% market share in 2024. The country’s leadership position is driven by its large expatriate population, with nearly 90% being immigrants who consider seafood an integral part of their traditional meals. The UAE has emerged as a hub for premium marine food products, with growing demand for high-value items like lobsters and scallops. The country’s strategic focus on aquaculture development, coupled with government support through fuel subsidies to the fishing sector, has strengthened its market position. The UAE’s sophisticated retail infrastructure, including temperature-controlled storage facilities and efficient distribution networks, has enabled better preservation and wider availability of seafood products. Additionally, the country’s status as a major tourist destination has boosted seafood consumption through its extensive hospitality sector, with numerous high-end restaurants and hotels offering diverse seafood cuisines.

GCC Seafood Market in Bahrain

Bahrain’s seafood market is projected to grow at approximately 2% CAGR from 2024 to 2029, making it the fastest-growing market in the GCC region. The country’s strategic focus on developing its aquaculture sector has been instrumental in driving this growth. Bahrain’s government has implemented comprehensive initiatives to boost local seafood production, including the identification of six strategic land plots dedicated to fish farming development. The country’s emphasis on sustainable fishing practices and investment in modern aquaculture technologies has attracted significant private sector participation. Bahrain’s unique geographical advantage, with its 161-kilometer coastline, provides excellent conditions for seafood cultivation. The country’s focus on research and development in aquaculture has led to the introduction of innovative farming techniques, particularly in breeding high-value species. Furthermore, Bahrain’s efforts to achieve food security through local production have resulted in increased investment in processing facilities and cold chain infrastructure.

GCC Seafood Market in Saudi Arabia

Saudi Arabia’s seafood market demonstrates robust development through its comprehensive National Fisheries Development Program. The country has established regional centers for fishing academies to support the fisheries sector, complemented by substantial investments in research activities to enhance production capabilities. The Saudi government’s commitment to developing the aquaculture sector is evident through its partnerships with international organizations and implementation of advanced technologies. The country’s extensive coastline of 2,640 kilometers provides significant potential for marine resource exploitation. Saudi Arabia has also focused on developing inland fisheries cultivation, with master trainers deployed to increase production efficiency. The market is further strengthened by the growing consumer awareness of seafood’s nutritional benefits and the increasing preference for protein-rich diets among the population.

GCC Seafood Market in Oman

Oman’s seafood market has established itself as a significant player in the GCC region, driven by its strategic location and access to rich marine resources. The country has successfully leveraged its traditional fishing heritage while embracing modern aquaculture technologies to enhance production capabilities. Oman’s focus on sustainable fishing practices and investment in aquaculture research has attracted international partnerships and investments. The country has developed sophisticated processing facilities and cold chain infrastructure to maintain product quality and extend shelf life. Oman’s market is characterized by strong domestic consumption patterns, with seafood being deeply embedded in the local cuisine and culture. The government’s support through various initiatives and subsidies has helped maintain the sector’s competitiveness and sustainability. Additionally, the presence of GCC company Oman in the region has further bolstered the market dynamics.

GCC Seafood Market in Other Countries

The remaining GCC countries, Kuwait and Qatar, contribute significantly to the region’s seafood market dynamics. These markets are characterized by their unique consumption patterns and development initiatives. Kuwait has focused on developing innovative aquaculture projects, including desert fish farming and improving existing aquaculture operations. Qatar has emphasized self-sufficiency in seafood production through various government initiatives and international collaborations. Both countries have implemented modern technologies and sustainable practices in their seafood sectors. The markets in these countries are supported by strong retail infrastructure and growing consumer awareness about the health benefits of seafood consumption. Their strategic location and access to marine resources continue to play crucial roles in market development.

Source: https://www.mordorintelligence.com/industry-reports/gcc-seafood-market?utm_source=chatgpt.com

Leave feedback about this